Tax-Deferred Annuity

One of the biggest challenges in today’s investment environment is withdrawing income from your portfolio or savings and not running out of money. Most long term averages since 2003 are 3% to 4% for diversified portfolios and pure fixed income like GIC’s and bonds are in the same range. Pure fixed income traditionally gets negative returns after taxes and inflation so most of us need some equities (ownership in companies) to offset inflation.

The problem with ownership of companies and even bonds in a rising interest rate environment is that we do not get a steady income. Withdrawals during the downturns do a lot of damage to the portfolios.

Income guarantees, inflation protection, and not giving up control, are three important retirement needs.

At 64 years old, John is planning on retiring this year and has approached our firm to discuss his options. He is looking for a strategy that can give him some income guarantees without giving up complete control of his assets. He is also concerned about inflation.

He has heard of life annuities and other products that give income guarantees for life but is concerned that these products may not give him access to his money should he need it, nor inflation protection.

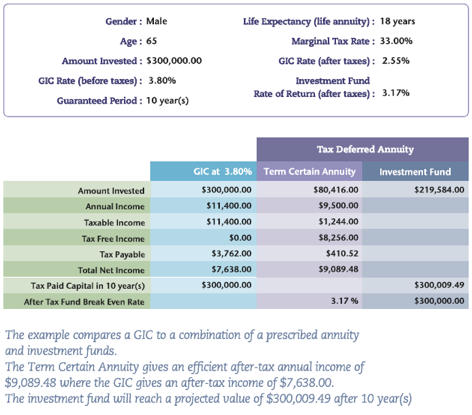

On top of his RRSP, John currently has $300k invested in a GIC from an inheritance (at 3.8%) that he would like to consider for his income needs. One of the options we presented to John was to consider using a 10 year term certain annuity.

A term certain annuity, in exchange for capital, promises to pay a known income for the next ten years. For example, $80,416 could purchase a 10 year guaranteed income of $9,500. Term certain annuities can be very tax efficient for non-registered investments and so in this same example, the gross income of $9,500 would equate to approximately $9,089 net of taxes (assuming a 33% marginal tax rate).

John could then take the remainder of his non-registered assets $219,584 ($300,000-$80,416) and invest that in an investment portfolio. For ten years, John would get his net income of $9,089 from his term certain annuity and his investment portfolio would grow uninterrupted. The portfolio would not be subject to the withdrawal damage during the dips. The investment portfolio could be set into a Corporate Class of investment which converts interest taxed at 100% into capital gains taxed at 50% giving him more money to keep by reducing taxes.

In order for John to have the same amount at age 74 as he initially had at age 64 ($300k), this investment portfolio would only have to return, over ten years (net of fees and taxes), 3.17%. If it returned more than this, the portfolio would be ahead. In the meantime, while not recommended, if John really needed to, he would be able to access funds.

At age 74, John would have two options, he could purchase another 10 year term certain annuity and start this strategy again for another 10 years or he could at that point purchase a life annuity. If the investment portfolio had greater returns than 3.17%, John could afford to increase his income allowing him to keep up with inflation.

By using a Term Certain 10 year Annuity and leaving his portfolio free to grow without making withdrawals John has received several benefits. He has guaranteed a tax efficient income for the next ten years; he has set his investment portfolio into a tax efficient growth position, but still has full liquidity. He has reduced taxes thereby reducing the likely hood of clawbacks on Guarantee Income Supplements, or Old Age Security at age 65.

John is also considering using a segregated fund investment portfolio which will allow him to place a 100% guarantee on his investment portfolio in event of death and or in 10 years. John is single and is also thinking about placing his daughter as beneficiary on the investment portfolio to avoid probate and will- based planning.

John’s enjoying his lemonade on the porch instead of watching the market news and worrying about his investments. Now that he left our office with a steady income and lower taxes and liquidity he’s got more important things to think about like his grandkids.